Housing market activity tracker Q2 2022

20 July 2022

It is hard to think of a more resilient market over the last two years, in the face of turbulence caused by lockdowns and economic uncertainty, than the housing market. Since January 2020, the average house price in England & Wales has increased by an average of 20 per cent. Supported by Government measures such as the stamp duty holiday from July 2020 – June 2021, as well as disruption to commuting habits, the housing market has undergone a unique period of intense change. However, with inflation nearing 10 per cent, interest rate rises continuing and the prospect of a UK recession, the housing market’s resilience is being tested again.

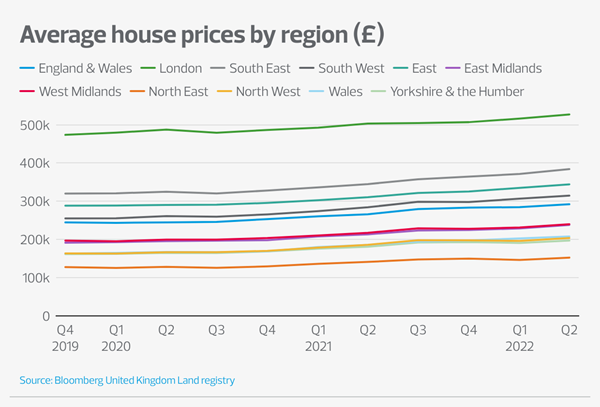

National and regional house price activity

Looking further into the house price changes over the year, this growth has not been evenly distributed. Since January 2020, the North West region has seen average prices rise by 23.5 per cent, the South East by 20 per cent and London by 10 per cent. As people left the cities and London in the ‘race for space’, demand for properties in more affordable areas skyrocketed, causing prices to inflate at an unprecedent pace. Many cash investors saw an opportunity to increase their portfolios, acquiring houses in the first-time buyer’s pool giving rise to a surge in the value of smaller dwellings. First time buyers struggled to compete with little flexibility in their high LTV mortgages as bidding wars began with cash buyers. Estate agents saw record highs of enquiries for properties with many properties sold before advertisement or viewings.

To combat the lack of supply, Government have set a target of building 300,000 new homes a year by the mid-2020’s. According to the Department of Levelling Up, Housing & Communities, only 216,490 net additional dwellings were added between April 2020 and March 2021, an 11 per cent decrease on the previous 12 months. In June 2022, government announced an extension to the Right to Buy scheme, with a separate pledge to build a new social home for every one sold. While this sounds good in practice, there have been no timescales announced and it will not make up the deficit between supply and demand.

While the Construction sector are innovating to deliver net-zero compliant new housing stock at speed, including through Modern Methods of Construction, there is a long way to go to meet demand and regulate prices. Completed new builds for the quarter October to December 2021 were 41,330, a 4 per cent reduction when compared to the previous quarter to September 2021 and a 11 per cent decrease when compared to the same period of 2020.

The mortgage market

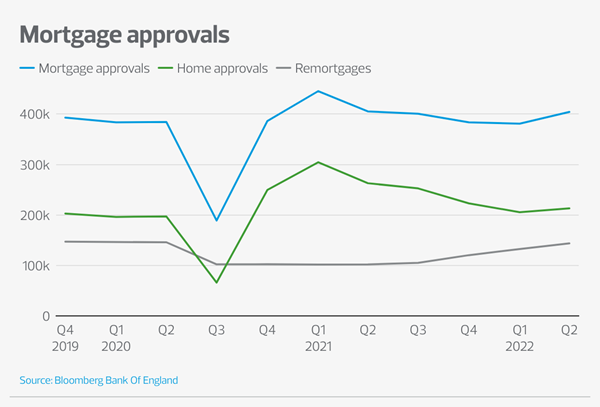

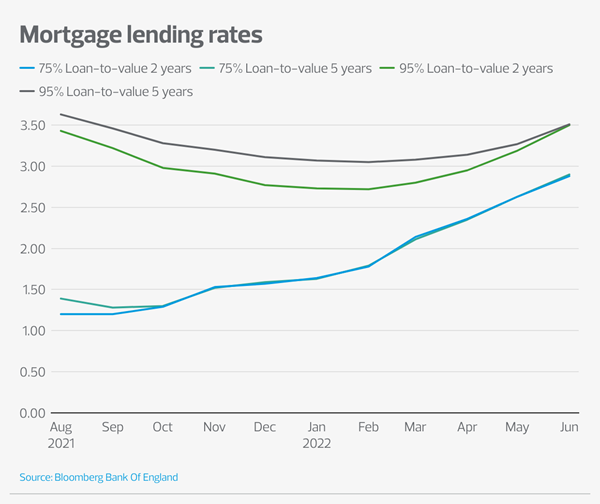

Mortgage approvals have been steady since Spring 2021, as buyers took advantage of historically low interest rates. The total number of approvals in Q2 2022 (404,288) was in line with Q2 2021 (405,259), which marked the end of the stamp duty holiday. However, the number of remortgages is trending significantly upwards as the below data illustrates.

In a potential boost to support mortgage approvals, The Bank of England are relaxing affordability tests from August, which should provide more flexibility for both lenders and borrowers. Borrowers are currently tested on whether they could afford mortgage repayments if interest rates were to rise by 3 per cent. This will be reduced to 1 per cent from August, which may allow some buyers to borrow more.

The UK interest rate has already risen to 1.25 per cent as the Bank of England attempts to stifle rampant inflation. The number of borrowers who have remortgaged early this year to lock in fixed rate deals is no surprise, despite in many instances the expected future rate rises already being priced in. There will be many borrowers on higher LTV bands still within fixed rate terms who will be concerned about where lending rates will be this time next year.

The Monetary Policy Committee’s (MPC) main focus is on preventing the current inflation shock becoming embedded in household’s inflation expectations, and leading to a wage-price spiral. However, the MPC must offset this against a weakening economy and the risk of a recession. Overall, we expect three more interest rate hikes this year of 25 basis points, which would take the BoE’s policy rate to 2 per cent. We then expect at least two more rises in 2023, meaning that interest rates will likely peak between 2.5 per cent and 3 per cent. However, the risk is that inflation proves stickier than we think, which would force the BoE to raise interest rates by more than we anticipate. On rates themselves, there is an interesting trend emerging when we compare rates offered for a Loan-to-value ratio of 95 per cent vs 75 per cent. While 95 per cent mortgage rates have remained broadly steady over the last year, 75 per cent rates have increased by 1.68 per cent. Lenders have therefore been raising rates across most of their lending book, rather than concentrate on riskier lending and pricing out would-be first-time buyers.

Steep rises in house prices and a flood of cash buyers into the market during the past two years has, for many first-time buyers, made the prospect of owning their own home an impossibility. The return of 95 per cent mortgages, the government’s help to buy scheme and stamp duty incentives has helped ease the burden of large deposits, but for many the affordability ratios continue to prove challenging.

One aspect of the housing market which will prove crucial to its stability is how those on a 95 per cent LTV mortgage fare in the event of a house price contraction. While a fall in house prices raise concerns over negative equity, the risk is not that of the 2008 recession. Lenders have limited their exposure with multiple providers offering 90 and 95 per cent mortgages, but at much lower volumes and the mortgage debt to income ratio remains much more stable than in the years leading up to 2008. More households have multiple income streams, less credit and more savings along with equity growth in their homes than that seen in the last financial recession. Many also have fixed term mortgages of 5–7 years secured when rates were at an all-time low.

Lenders actively increased mortgage debt availability during the pandemic to aid the government incentives to support first time buyers and renters looking to become owners. The government backed 95 per cent mortgage scheme and reduction in LTV across the total mortgage debt book has reduced the risk to lenders and likelihood of a financial crash for the housing market.

National Housebuilders have set plans to increase volumes following an increase in orders last year. However, with further increases to material, energy and labour costs anticipated, coupled with a slowdown in the market, this could mean a fall in new build house prices squeezing margins for the industry. Thankfully, this is unlikely to have a severe impact on the housing market as demand and government targets for new homes and affordable homes continue to increase.

RSM’s predictions

- While house prices have begun to stabilise, it is unlikely we will see a major contraction in the volume of house builds and sales.

- Housebuilders and social housing organisations will continue to increase volumes built to meet a backlog of demand for housing targets not meet in earlier years.

- House prices will fall slightly in 2022, which will be a moderate correction of the market increases seen during the pandemic.

- Lenders are unlikely to remove 90-95 per cent LTV mortgages as government continues to support first time buyers and encourage renters to buy their own property.

- Increased volume of fixed term mortgage > 2years will be seen as borrowers lock in interest rates.

- Interest rate increases are forecast to peak at around 2.75 per cent by the middle of 2023 before levelling off. While they may rise a little bit beyond that, they are unlikely to get to the 5 per cent that was common before the Global Financial Crisis.

Related insights

Ec test Dec2023

13 Dec 2023

Consumer Duty readiness survey

19 Apr 2023

Housing activity market tracker Q4 2022

08 Feb 2023

Ec test Dec2023

13 Dec 2023

Consumer Duty readiness survey

19 Apr 2023