Semi-conductors – tiny components in enormous global supply chains

For many businesses suffering from backlogs in their supply chain, it is the availability - or rather non-availability - of semi-conductors that is to blame. As with many things in life, the devil is in the detail. These tiny components (often measured in nanometres) are ubiquitous in infrastructure for the production of goods and delivery of services. After enormous disruptions triggered by the pandemic, the US Government and European Union have announced radical plans support their semi-conductor industries in order to protect supply chains. By comparison, in the UK, many are concerned that more should be done to protect our own businesses against over dependence on other countries’ supply chains, even though our industry was a world leader back in the 1970s.

Not enough chips

Only when there was a scarcity of semiconductors did we realised how vital they have become. Microchips are integral to so many aspects of daily life; computers, handheld devices, gadgets, robots, telecoms systems and automobiles.

It was early in the pandemic that the chip fabrication facilities were shut down. This, combined with a rising demand for chips for consumer electronics and telecoms, has caused an acute supply chain issue.

The automotive industry was hit particularly hard. As automobiles have become increasingly more complicated, they require more chips. A lead time of over a year is now not unusual for a new vehicle leading to the costs of second-hand vehicles to soar.

However, whilst the travails of the automotive sector are well published it only constitutes approximately 9 per cent of a global market that was valued at $529bn in 2021. That valuation is expected to rise to $735bn by 2026.

Over 60 per cent of the market feeds two pillars that are crucial to the growth of all middle-market businesses - computing and wireless telecommunications. These key segments make up 33 per cent and 31 per cent of the market in 2021 respectively. Wireless communications are anticipated to continue to grow as advancements in areas such as 5G and satellite internet increase global connectivity and support emerging trends such as Web 3.0 and the metaverse.

Semi-conductors are likely to be even more important in the future than they are today.

Investing to stay ahead

To the global leaders in manufacturing, enormous investment will likely yield high rewards. In January 2022, Taiwan Semiconductor Manufacturing Company, the world’s biggest contract manufacturer, said it would spend up to $44bn on new capacity in 2022. Samsung announced spend in 2022 will surpass $33bn. In the United States, Intel plans to spend $28bn, including two new factors in Ohio by 2025 at a cost of $20bn.

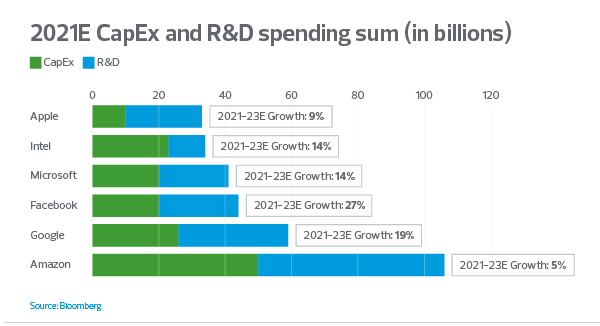

BigTech’s ambitious plans will drive the need for more chips. At the outset of 2022 the ‘Big 6’ announced ambitious capital and R&D spend to drive their business growth, all of which will contribute to the increasing demand for semi-conductors. This sits alongside trends such as autonomous and electric vehicles, greater connectivity within infrastructure and advancements in new consumer electronics such as headset and handheld devices to access virtual and augmented reality.

The US takes steps to protect its supply chains

Whilst chips are designed all over the world, the vast majority of fabrication takes place in Asia, with manufacturing giant China having the greatest manufacturing capacity of all.

Semi-conductors are particularly crucial to the United States. The Semiconductor Industry Association have reported that in the US R&D expenditure as a percentage of sales ranks 2nd at 18.6 per cent, surpassed only by pharma and biotechnology (27.1 per cent). Their estimates of US semi-conductor R&D rank it as number one globally.

In the United States the government earmarked $52bn in subsidiaries for chip companies. The onshore manufacturing of chips was identified of crucial importance with $10bn earmarked for the construction of fabrication facilities. In funding the announcement they declared that the US has outsourced and offshored too much in the past 10 years, including their semiconductor production. They believe that this loss of chip manufacturing capacity threatens their international competitiveness.

Even with the significant investment announced, it is China who is projected by analysts at Bloomberg to continue to be the global leader in fabrication capacity with monthly capacity of almost 4.7 million by the end of 2023- approximately 23 per cent of global production. This is balanced against projections that China will account for approximately 28 per cent of the global market by the same point.

The United States by comparison is expected to have capacity for 2.9 million units a month by 2023 – approximately 10 per cent of global production. Projections estimate the United States will account for 27 per cent of the global market at this point. Whilst the US will be able to source chips from Asia, the need to protect its supply chain from global disruption is clear.

Investment in Europe and the UK falls behind

Turning to Europe – EMEA is expected to constitute approximately 21 per cent of the global market. European fabrication capacity is expected to be 10 per cent of global capacity in 2023. Europe therefore, faces the same challenges as the United States.

The European Union moved to protect its supply chain with the European Chips Act unveiled in February. This made an additional €15bn available to chip manufacturers. This is in addition to €30bn previously outlined. Data from SEMI indicates Germany’s fabrication capacity of 200mm wafer equivalents is expected to rise to 878,556 a month by 2023. France is projected to rise to 616,400.

The United Kingdom lags behind many European countries, with anticipated monthly capacity of 200mm wafer equivalents 173,430 by 2023. Over half of this capacity is based in South Wales – a hub of semi-conductor activity. Close neighbours, Ireland is projected to have greater capacity than the UK at 230,500.

For some in the United Kingdom, there are concerns over the lack of recognition from the Government of the need to fund and build its own fabrication facilities. The UK has strength in the design of semi-conductors, but is exposed to overseas supply chain risk.

Bracing for the ongoing shortages

Many mid-market businesses will have had their operations disrupted during or after the pandemic by the shortage of silicon chips – ranging from the unavailability of key IT equipment to replacing the company car fleet with cost effective EVs. The demand for chips over time is expected to increase globally as more chips are required to drive advancements in technology.

The United Kingdom’s relatively small capacity for manufacture of chips does appear to significantly fall behind some of our European neighbours, which may leave the country exposed to hiccups in overseas supply chains. However, the growing industry in South Wales does provide a glimmer of hope – but this sector will need support and protection from the Government, similar to the efforts being made in the United States and the European Union.

Manufacturers will already be aware of the need to consider the origin of components in their supply chain. However, boards in all industries may want to consider the role of microchips in key investments. For example, organisations may want to plan ahead and build contingencies into their IT refreshment cycles to anticipate unexpected delays of key parts. As energy costs rise, delays are almost certainly to be expected when procuring electric vehicles to replace the company car fleet.

The Real Economy

Subscribe to The Real Economy

Related insights

Shock proofing retail supply chains

02 Aug 2022

How to future proof your supply chain

14 Jul 2022

UK inflation: running up that hill

14 Jul 2022

Shock proofing retail supply chains

02 Aug 2022

How to future proof your supply chain

14 Jul 2022