2023 to be a tough year for consumer spending

16 January 2023

The record-breaking drop in household’s real incomes in 2022 and 2023 means that consumer spending is heading for a sharp fall this year after dropping by 1% q/q in Q3 2022.

As you might expect, spending on most discretionary areas, such as clothes and household goods, has fallen sharply recently as the cost-of-living crisis has caused consumers to cut back. However, more surprisingly, spending on hospitality services has continued to grow over the last three quarters, despite the huge headwinds as consumers have favoured experiences over goods.

However, we doubt the resilience of hospitality spending will continue in the face of a near 2% drop in real incomes this year. Indeed, with consumer confidence near a record low, meaning that consumers are still adding to their pile of excess savings rather than spending them, we think total consumer spending will fall by about 2% in 2023.

The good news is that inflation should fall rapidly this year reaching 4% by the end of the year, or even lower if the recent falls in energy prices are maintained. That means households real incomes should be rising again by the end of this year, setting the stage for a decent recovery in 2014.

Consumers are too scared to spend their savings

The outlook for consumer spending generally depends on two things; how much money consumers have to spend, and how willing they are to spend it.

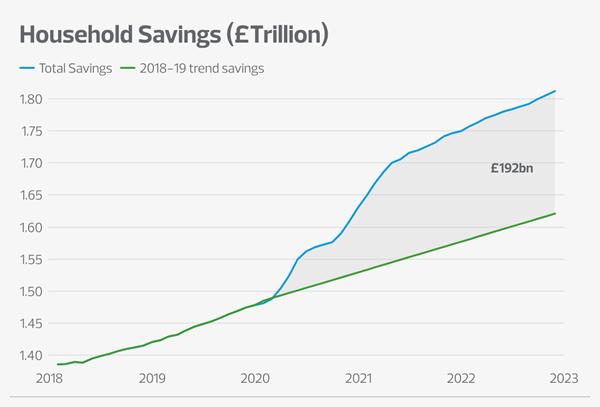

Households entered the current recession in relatively good shape. Households have accumulated excess savings of almost £200bn (about 10% of GDP). What’s more, at just 3.7% the unemployment rate is historically low and wage growth of 6.1% y/y is exceptionally high, at least in nominal terms.

The strength of balance sheets, low unemployment rates and high nominal wage growth should have allowed consumers to continue spending through the cost-of-living crisis, shielding the economy from a 1990s style recession.

However, there are three big problems. First, the surge in inflation to double digits has meant that even though nominal wage growth is rising strongly at over 6% a year, real earnings are plummeting by about 5% y/y.

Second, consumer confidence has collapsed to record lows. As a result, households have continued to build their excess savings rather than spend them. Indeed, the household saving ratio, which measures the proportion of their income that households save, rose from 6.7% in Q2 to 9% in Q3.

Third, the unemployment rate is low because employment is still about 0.5% below its pre-pandemic level. The reduction in employment and subsequent lower incomes directly feeds through into lower overall consumer purchasing power.

Admittedly, we expect inflation to fall from 10.7% currently to about 4% by the end of 2023, which will give a substantial boost to real wages. And in a rare bit of positive news natural gas and electricity prices have recently fallen below their level at the start of the Ukraine war. This could mean that government could be minded to cancel April’s scheduled Energy Price Guarantee rise in the upcoming budget in March. If the EPG stays at £2,500, CPI inflation will likely be 1 percentage point lower by the end of 2023 and household’s real incomes would be 1ppt higher.

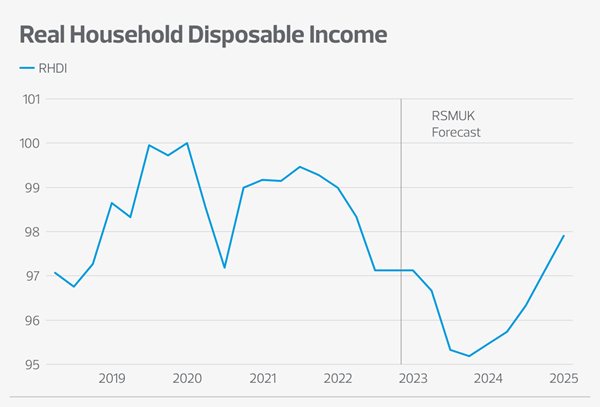

But adding up all these factors, we expect Real Household Disposable Incomes (RHDI), which is the main measure of the purchasing power of the UK consumer, to fall by about 1.8% in 2023 after a similar fall in 2022. That’s by far the biggest fall on record.

The impact of higher interest rates

It may seem strange that we’ve waited until now to mention soaring interest rates. That’s because higher interest rates have little net impact on aggregate RHDI. Mortgage rates and other interest costs rise but higher interest rates also boost interest income on household savings, and the impacts of these changes broadly offset in aggregate as the stock of household deposits is roughly equal to the stock of debt. However, it does matter for consumption because those adversely affected by higher interest rates are likely to cut spending by more than those who benefit from higher interest income.

The outlook for consumer spending

We’ve established that consumers real incomes are set to take a massive hit this year and that consumer confidence is so low that most are trying to save more, rather than run down their savings. All this makes it inevitable that consumer spending is also going to take a bit hit.

We that after rising by almost 5% in 2022, total consumer spending will fall by about 2% in 2023.

But which industries will be hit hardest?

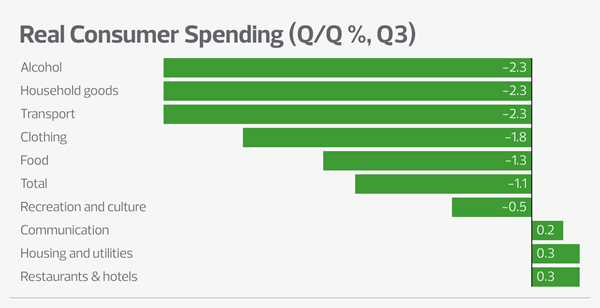

Over the last year consumers have cut back significantly on certain types of discretionary spending. Spending on clothing fell by 5.7% in Q2 and 1.8% q/q in Q3 and the volume of household goods dropped by 1.7% q/q in Q2 and 2.3% in Q3. Consumers have even been cutting back on essential items, food sales have fallen for three consecutive quarters and transport spending dropped by 2.3% q/q. However, hospitality spending has, so far at least, held up well. Spending on recreational and cultural activities was relatively flat in Q3 and spending on restaurants and hotels even rose slightly. This suggests that consumers are prioritising experiences over goods, a reversal of the pandemic years.

The early signs are that spending in Q4 held up reasonably well, helped by mild weather for most of it and a desire for a “normal” Christmas after Covid disrupted the previous two. However, given the scale of the hit to real incomes we envisage this year, it seems likely that spending on hospitality will also start to fall soon.